Long-term value of $1 invested vs. long-term value of $1 saved

There is a difference.

Should you save? or should you invest? When you were little, you may have heard that you should save some money for a rainy day. While it is always good advice to have money that you can dip into if/when needed, that is not necessarily the best advice for money that is excess of what you need for your expenses and emergency fund. You also need to invest your money. But how many of us are told that at an early age? There is a difference between investing and saving and you must know the difference between:

The long-term value of $1 invested vs. the long-term value of $1 saved.

There is a sizable difference over time of what you can expect to get for your money if you invest it in assets - like stocks - versus if you save it - like in a checking or savings account.

Why is this so important? Because you want your money to work for you.

This concept is really important to understand because we have been taught - from a young age - to save our money for a rainy day, but it is rare where someone has told us to invest our money, especially as women. And there is a difference between saving and investing that manifests itself over a longer period of time. Because the less money you have invested, the less money you will get versus someone who invested more over the same time period.

Your choices

Upfront you need to have money that you can use to pay your expenses. And you should also absolutely have an emergency fund. (Need more info on what to do before you invest? Get our free pre-investing workbook). But when you have money that you don’t need to pay expenses and you already have an emergency fund, you have several options for what you can do with the “excess” - namely you can save it or you can invest it.

If you save it, that one dollar will likely stay in a checking or savings account. If you invest it, that one dollar will go into an asset class, let’s assume the stock market.

Which one do you think will give you a greater return down the road?

Let’s look at the math.

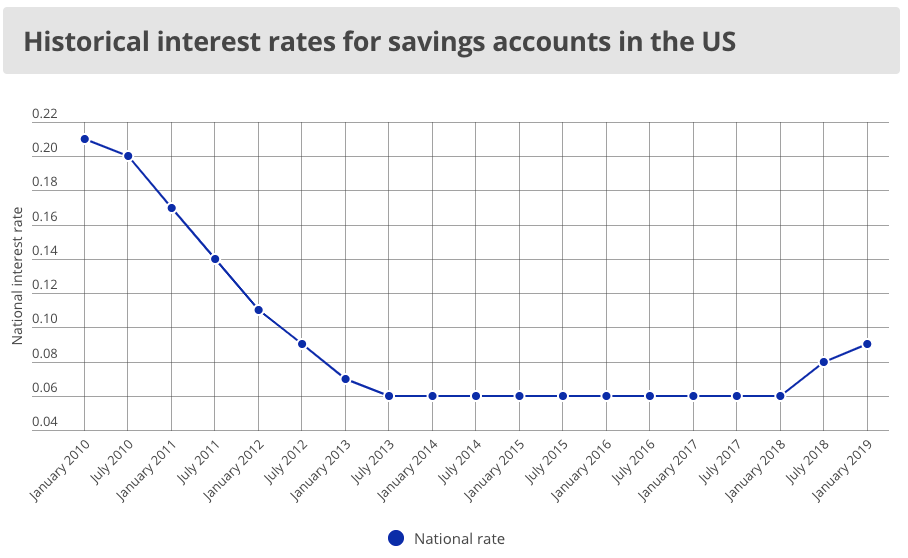

Historically, the savings interest rate for savings accounts is very low.

Let’s assume that the savings account interest rate is 1%, as there are some higher yield accounts available. So, assume that your $1 will earn 1% in a savings account.

If you save that $1 in a savings account at a 1% interest rate and don’t touch it for 20 years, what will you have at the end of that time period?

You will have $1.22.

Now assume that instead of saving that $1, you decide to invest it. Let’s say you invest it in the S&P500 Index, which has had an average annual rate of return of around 8%.

Right away you know that you will have a greater return by investing the $1 than by saving it. Why? Because an 8% return is greater than a 1% return. But let’s do the math anyway to see just how much of a difference there is in returns to you.

The difference in returns is drastic!

When you save the $1, you get $1.22 back in 20 years!

When you invest the $1, you get $4.66 back in 20 years!

This is a simple example, but it illustrates the power of investing that $1 versus just saving it.

Now, we haven’t even accounted for inflation – which reduces the value of your money over time.

What is inflation?

Inflation: the general rise in the price levels over a period of time. Because there is an increase in prices, it will cost more today to purchase the same level of goods or services you could purchase a year ago, simply because the prices of those goods or services increased.

For example, let’s say in year 1, you purchase a loaf of bread, a carton of orange juice, and a carton of eggs. This all costs you $12.

Now, let’s say in year 3, you decide to buy the same exact goods. But now it costs you $15. That $3 difference is inflation. Basically, it costs you more money now to buy the same goods that it did three years ago.

So, what does this mean for you?

This means that the purchasing power of your $1 goes down over time - the same $1 buys less over time. So what do you need to do?

This means that you have to have your money work for you – but in a way where it will beat inflation.

If you let your money sit in a savings account, earning nominal interest rate, you will lose money just by keeping your money there.

What? Why?

Take an example. Inflation is typically around 2-3%. If you earn 1% per year, but you lose the value of your money by 2% due to inflation because the prices of goods and services are going up on average by 2% per year, then you are at a net loss of -1% of your $1 in a year and you have thus, lost money by keeping it in a savings account. In other words, your savings has not increased enough to offset the inflation loss.

This means that for every $1 you have in a savings account, you would really only end up with $0.82 in 20 years because of inflation. To be clear, that $1 does not decline to $0.82! But the amount of goods and services that your $1.22 can buy at the end of 20 years effectively represents what $0.82 could buy you in year 1.

But if you invest your money in the stock market and you earn 8% a year, then you are beating inflation of 2-3% per year and your money is working for you, and you end up with $3.21 at the end of 20 years, even with inflation at 2%.

See the difference? You would get $3.21 even with inflation if you invest your money vs. the equivalent of $0.82 if you save it. Investing is powerful!

Of course, there are risks when you invest and you should understand those risks as well. But you absolutely must know the difference between savings and investing your money.

Key: Know the long-term value of your dollar if you save it versus the long-term value of your dollar if you invest it.

Check out our website SHALnCO for more resources on investing, including courses and eBooks.